Why London’s property market is stagnating

When my wife and I were deciding where to make our long-term home, we flipped a coin. Heads, we’d stay in London. We had both moved to the city to study in the early 2000s; it’s where we first met and I started my career. Tails and we’d move to the South West.

The coin came up heads. But in the moment of flipping, we both realised we preferred the idea of moving away. Bath is where we ended up.

At the time two things occurred to me: first, we were following a well-worn trend; one that, since the second world war, has consistently seen more Brits leaving London than moving to it; and two: since house prices grew much quicker in London than anywhere else, we were effectively committing ourselves to the “slow lane” in the UK’s two-speed property market. In all likelihood, we’d never be able to afford to buy ourselves back into the city.

Or so we thought. Because, 15 years later, while the capital still has by far and away the most expensive homes in the country, this masks something that you rarely read about: London’s property market has been stagnating for years.

In the past decade, London house prices have increased by just 13 per cent — that amounts to a 16 per cent fall in real terms. For the city’s average house price you could buy 2.4 homes in the North West. Back in 2016, it would have bought you 3.4 homes.

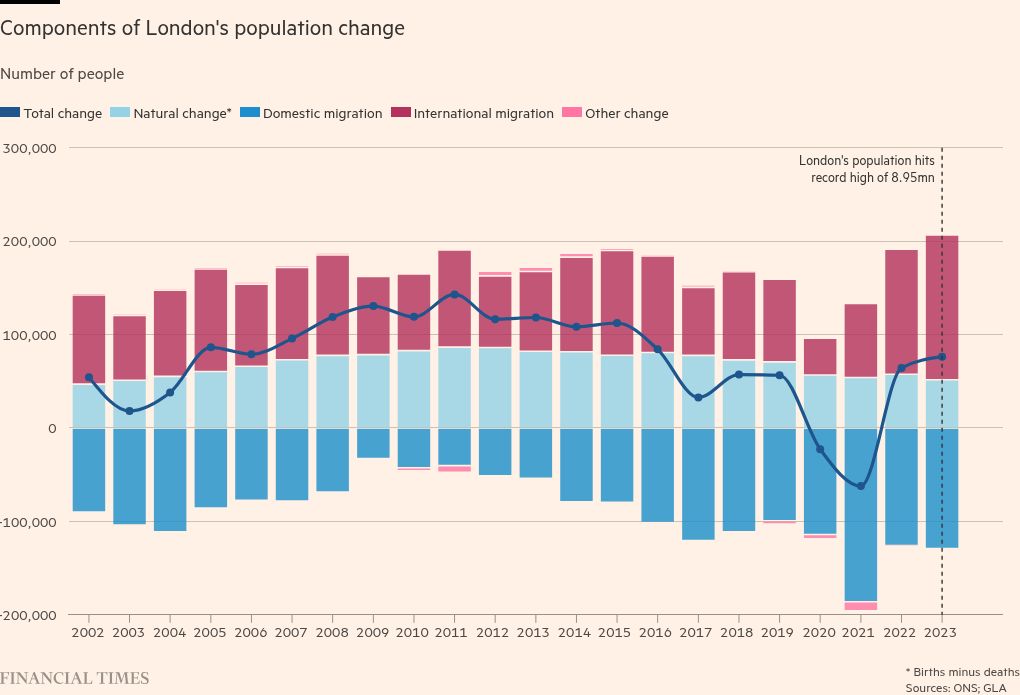

The irony is that demand for London homes has never been higher. After riding out the slump caused by Covid, the city’s population hit a record high in 2023, with 8.95mn people. Given that the ONS has recently increased its UK net migration estimates for the 12 months to June that year — and that London always attracts a large share of international migrants — there’s a good chance its population hit another record high six months ago. While this has helped drive up rents to record levels, it’s barely touched the sales market.

So how has this happened?

Usually, London takes the lead during the early stages of a housing market cycle. Growth starts in the centre before spreading out across London and, if the cycle lasts long enough, might reach somewhere like Kilmarnock. During the early stages of the cycle, younger homeowners in London build up equity in smaller homes before trading up into more affordable locations further afield — in turn helping to spread the market cycle.

This happened after the financial crisis, as international investors flooded in looking for a bargain in Belgravia, Kensington and Chelsea. Price increases rippled outwards, first to the South East, and then to large parts of the rest of the country.

But the last eight years have seen London house prices stultify, weighed down by declines in its posh central areas.

The recent stagnation, especially in outer, more affordable parts of the city, can be clearly tied to the rise in interest rates: London’s high prices make the market more dependent on high loan-to-income mortgages and landlords have to put up with much lower rental yields, compared with the rest of the country. Without a correction in prices, we’ve ended up in a stand-off where few people can afford or are willing to buy while even fewer need to sell.

The longer-term stagnation is more complex, but its beginning offers some clues. First the reform of stamp duty in December 2014 made it much more expensive to buy higher-value properties.

This started the slowdown in central London but was quickly added to by the introduction of the additional higher rate on additional dwellings tax in March 2016 along with tougher regulation on buy-to-let mortgages and the phased removal of interest relief for higher-rate paying landlords from 2017.

All of which have reduced the attractiveness of buying investment properties, particularly in markets with very low rental yields where the priority tended to be capital appreciation as long as the rent covered costs.

But it’s not just landlords who have been affected by a tougher lending environment. London’s first-time buyers have been hit hardest by the introduction of both the mortgage stress test and the flow limit on lending above 4.5 times incomes. These have combined to create a situation where you can only buy if you have a massive deposit — £144,500 on average, according to UK Finance.

So, unlike the rest of the country, where first-time buyer numbers actually recovered to pre-financial crisis levels, in London they fell away in 2014 and didn’t even manage to hit their previous peak during the post-pandemic mini-boom. Inevitably, given mortgage rate rises, numbers have fallen further since then.

While a period of no or low house price growth while incomes catch up might look like the ideal solution to stretched affordability, even this is not cost-free. The recent surge in international migration and reduced first-time buyer numbers have contributed to London’s record rent rises. Meanwhile, those who have managed to buy their first home will find it harder to build up equity and may even find themselves trapped in homes that are too small, with some facing the additional challenge of dealing with the cladding crisis or finding it difficult to sell their shared ownership home.

The low levels of transactions are more of a concern, since it can lead to the inefficient use of the housing stock, reduce labour mobility and lower the government’s tax-take. It also has an impact on the number of new homes being built, given many have been targeted at either buy-to-let investors or first-time buyers via Help to Buy.

Even the emergence of a new type of buyer, institutional Build-to-Rent landlords, couldn’t stave off a drop in housing delivery. Last week’s data from the government showed that London added just 32,162 homes to its housing stock in 2023-24, the lowest level since 2014-15.

So far, attempts to de-zombify the London market look impotent. Longer-term mortgage products and those with higher income multiples might help some on the fringes, but their supply is going to be constrained and they’re going to suit even fewer. The price war between lenders has abated too, with mortgage rates back up above 4 per cent again.

The question for policymakers is how they can boost activity without inflating house prices — taxing people’s homes might work in theory but the political fallout would not be pretty, and funding for the number of new homes required is a difficult challenge that will require more money. And we’ll have to wait even longer to find out who’s getting any given the delay to the Spending Review.

Moving away from the capital comes with plenty of compromises. Learning to keep an eye on the time when spending an evening out in London so you didn’t miss the last train was a skill I had to learn early. But, at least for me, the benefits of living in the South West outweigh those of London. The coin chose wrong and we got it right. Even the data is starting to agree.

Neal Hudson is a housing market analyst and founder of the consultancy BuiltPlace

#Londons #property #market #stagnating