How the world’s biggest offshore wind company was blown off course

As the Danish renewable energy company Ørsted battled to restore its reputation following a bruising year, a rival across the North Sea had the company in its sights. After months of quietly buying Ørsted shares, Norway’s state-owned oil and gas giant Equinor revealed in October that it now had a 10 per cent stake, promising to be a “supportive” shareholder.

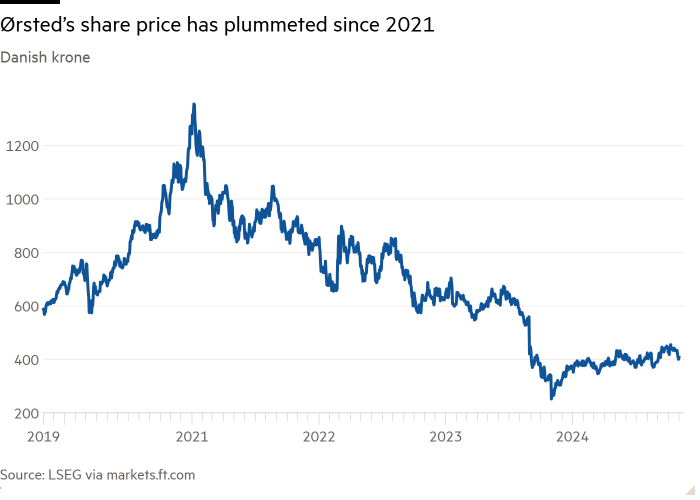

The move was hardly unusual in Europe’s fiercely competitive energy market. At one level, it was a vote of confidence in Ørsted, whose value has fallen roughly 70 per cent since 2021 amid management mis-steps and a challenging economic backdrop. And it enabled Equinor to continue its own journey towards decarbonisation on the comparative cheap, making up for a slow start.

But it spoke volumes that a Norwegian competitor still heavily attached to fossil fuels — the previous year, 20 per cent of Equinor’s investment was in renewables and carbon capture — was buying a chunk of Ørsted, the world’s largest offshore wind company in terms of operational capacity, which had become a proud symbol of Denmark’s transition to low-carbon energy.

Ørsted’s journey over the past 15 years, from fossil fuel driller to a renewables pioneer, reflects the remarkable evolution the energy sector has experienced as the world battles to decarbonise.

It also illustrates how the push for rapid growth in the sector to meet climate goals has met economic, political and practical hurdles. After struggling with rising costs, the company has had to abandon and pause significant projects, not only in offshore wind but in hydrogen and green fuels.

Many of its European peers have likewise been chastened as the era of ultra low-cost borrowing ended, the ESG investment boom fades and the push for clean power has become snarled in queues to connect renewable sources to the electricity grid.

Investors point out that renewable energy is still on a strong path. Some 565 gigawatts of new renewable electricity plants were added last year, the fastest pace in two decades — driven largely by the huge expansion of solar power in China.

And the sector is increasingly cost-competitive. When it comes to Ørsted’s specialism, offshore wind, the global average cost has fallen to $81 per megawatt hour, down from $137 in 2018, according to the most recent data from BloombergNEF. That compares with $72 per MWh for coal-fired power plants and $83 for gas-fired power plants, respectively — figures unthinkable just a few years ago.

“Renewables growth used to be based on climate targets; now it is very strong economic logic,” says Martin Neubert, formerly Ørsted’s deputy chief executive, now group chief investment officer at renewables investment giant Copenhagen Infrastructure Partners.

Yet Ørsted’s shares slumped again last month when Donald Trump was re-elected. The event has sent another earthquake through the energy industry and has made the shift away from fossil fuels seem suddenly less certain, at least in the near term.

The president-elect, who has called climate change a “hoax”, has pledged to put a stop to key Biden-era green subsidies and pull the US out of the Paris Agreement. He has also threatened to scrap offshore wind projects on “day one” and impose higher tariffs that would push up the costs of green tech.

Analysts are waiting to see whether he will follow through, but what is already clear is that the path to green energy is more circuitous and far bumpier than many hoped. “We increasingly fear our road map to net zero is not what will happen,” research consultancy Thunder Said Energy said in a recent note, pointing to problems such as limited willingness to pay for decarbonisation, fractious global politics and slow progress in developing carbon capture.

Ørsted’s own transformation has its roots in the run-up to the international UN climate change conference in Copenhagen in 2009. Denmark’s national energy company was then known as Dong Energy, and its oil and gas wells and coal-fired power stations accounted for about a third of the country’s entire CO₂ emissions.

The conference left a lasting mark on Anders Eldrup, a former top civil servant in Denmark’s finance ministry who was then Ørsted’s chief executive. Before it even began, he announced a plan for the company to produce an ambitious 85 per cent of its electricity and heat from renewables by 2040, up from 15 per cent at the time. Although some on the board had doubts, Eldrup was determined. “It was the right thing to do, and it was also good business,” he says.

State support, high wind speeds in the North Sea and the fact that turbine makers Siemens Energy and Vestas were based near by made the nascent offshore wind sector seem like a good bet. Ørsted pushed the industry forward, developing ever-larger farms such the Hornsea 1 project off the Yorkshire coast — the first globally to exceed 1GW capacity, which started generating in February 2019.

“At the time, there was not much competition, feed-in-tariffs [subsidies] were pretty high, and Ørsted was a first mover,” adds Eldrup.

Ørsted also converted some of its power stations to run on biomass — mainly wood chips and pellets — instead of coal. Although controversial with many environmentalists, the fuel is counted as carbon neutral in Denmark and other countries if it is sustainably sourced.

Jonathan Cole, chief executive at the rival Corio Generation, owned by the Australian asset manager Macquarie, says that the company was innovative in another way too: financially. “They were one of the first big utility industrial players to find a way to work with institutional capital and bring them in early on,” he says. Over the decade up to 2018, it and its partners invested DKr165bn ($23.2bn) in green energy.

Mads Nipper, Ørsted’s chief executive, says the company has to “some extent been like the Tesla of offshore wind . . . proving that scalability was possible to an extent that nobody thought possible”.

In 2017, a year after it listed in Copenhagen, the company sold off its oil and gas production business to the chemicals empire Ineos for just over $1bn. It was also rechristened in honour of the 19th-century Danish physicist Hans Christian Ørsted, who discovered electromagnetism (a lawsuit from Ørsted’s descendants objecting ended up in Denmark’s Supreme Court).

In 2018, the company reported that its electricity output was 75 per cent green, substantially ahead of target. Emissions per kilowatt hour were cut by 64 per cent in just four years.

This progress matched huge growth in renewable electricity capacity more widely, helped by ultra-low interest rates. Between 2010 and 2020, 644GW — enough power to supply hundreds of millions of homes — was built globally. Meanwhile, production costs fell between 48 per cent and 85 per cent depending on the technology, according to the International Renewable Energy Agency.

By late 2020, Ørsted’s valuation reached £51bn — higher than BP’s, even though it produced a fraction of the energy. But the hype did not last. In the years following the pandemic, as interest rates jumped, supply chains came under strain and investors looked at higher returns elsewhere, Ørsted and others came under increasing pressure.

To secure financing — a challenge for renewables companies, where costs are heavily front-loaded — many had already locked in electricity prices on large projects. That was a particular problem in the US, where Ørsted also overestimated its ability to get tax credits from the federal government. When the company warned in August 2023 that discussions were not progressing well, investors began to worry.

Early that November, when Ørsted said it would walk away from two huge offshore wind projects in New Jersey, triggering some $4bn in impairments, its shares tumbled almost 30 per cent.

The subsequent 12 months have been rough: the company announced that its finance chief and chief operating officer would leave, a suspension of dividends, a downgrade to its renewables target to 35-38GW by 2030 (a reduction from 50GW) and up to 800 job cuts.

It also pulled out of offshore wind markets in Norway, Spain and Portugal. “It was an annus horribilis,” says Tancrede Fulop, senior equity analyst at Morningstar.

Executives insist one bad year for a company does not herald a long-term crisis — electricity prices have risen to cover higher project costs and supply chains in many markets have adjusted.

Yet analysts point out that Ørsted is not the only energy business to have experienced difficulties, and that the sector is more fragile than first appeared. “Depending on how you measure it, clean energy is five to 10 times more sensitive to changes in interest rates [than fossil fuels],” notes Nick Stansbury, head of climate solutions at Legal & General Investment Management.

Statkraft and EDP are among European utilities to have trimmed this year’s targets for new renewable electricity projects, with Statkraft’s chief executive, Birgitte Vartdal, highlighting “challenging” market conditions. Other offshore wind developers such as Equinor and Vattenfall have also pulled back from expansion plans.

Costs may have fallen, but Stansbury questions whether that can continue. “Improvements from here may be much more modest than previously thought,” he says.

RWE, the German energy giant, said last month that it would spend less on green projects next year compared with this, instead choosing to buy back €1.5bn of shares. The company cited risks to offshore wind in the US given Trump’s threats, as well as delays to the development of Europe’s green hydrogen industry, a big potential consumer of renewable electricity.

The EU has introduced ambitious targets for producing and using hydrogen. But, again, high costs and insufficient infrastructure — as well as limited demand — have held the industry back.

Investors highlight the hurdles facing less mature technologies. “We are now in a very different economic environment,” says Ralph Ibendahl, global head of energy transition at RBC Capital Markets. “There’s just less capital available.”

Analysts at Jefferies say the energy transition is in a “new defining phase”, adding in a recent note: “Macro conditions have changed markedly, technologies and business models are hitting inflection points, scale is materialising for some, whilst there will be false dawns for others.”

The shift has created opportunities for those who can afford to take a long-range view, such as the UAE’s clean energy vehicle Masdar, which has recently scooped up European wind and solar farms, aiming for a 100GW portfolio by 2030 — twice Ørsted’s original target.

Nicolai Tangen, chief executive of Norway’s sovereign wealth fund, which is a top-three shareholder in Ørsted, says the “ESG backlash” means there are fewer competitors for renewables projects, but that offers attractions for investors. “We see broad opportunities,” he adds.

Set against this, of course, are the realities of global warming. Despite the surge in renewable generating capacity during 2023, energy demand also rose and emissions hit a record high of 37.4bn tonnes. In the global energy mix, fossil fuels’ position has not fallen much over the last two decades, still making up more than 80 per cent of all energy consumption.

After the more than 60 per cent growth achieved in 2023, the International Energy Agency expects renewable power to expand at 20 per cent this year. The IEA has upgraded its expectations for renewables capacity by the end of the decade to 9,765GW — a figure that falls short of the 11,000GW target set out at last year’s international climate summit, COP28. And it warns the pace is still not fast enough.

To be on track for net zero emissions, its analysts said in October, clean power needed to grow “1.5 times faster in China, 1.9 times faster in advanced economies, and three times faster in the other emerging market and developing economies”.

Even so, Kingsmill Bond at the RMI think-tank is optimistic. He points to rapid growth of solar power, batteries and electric cars, and cost competitiveness. “Cleantech deployment and investment is continuing to move up an S-curve and will dominate spending by 2030,” he argues.

Meanwhile, a growing proportion of experts are optimistic that China’s emissions have peaked or will peak next year, according to a survey in November by the Centre for Research on Energy and Clean Air. That would mark a significant turning point.

“The door is open,” adds Bond. “The question now is, can the politics hold back the economics?”

For its part, Ørsted is busy trying to restore its credibility, focusing on meeting its reduced target of 35GW to 38GW of renewables capacity by 2030. Some 60 per cent of this will come from offshore wind, the rest from onshore wind and solar. And it has signed off large investments in batteries to store electricity from its wind farms.

It is also trying to raise about DKr115bn ($16.1bn) by the end of the decade by selling stakes in wind farms and other assets. Last month it sold a 12.45 per cent stake in four of its UK wind farms to the Canadian infrastructure giant Brookfield for about £1.75bn. The next test will be the sale of a stake in its giant Hornsea 3 offshore farm, an £8.5bn project it is developing off the Yorkshire coast, in the new year.

“They have a plan to get out of the woods,” says Deepa Venkateswaran, head of utilities at Bernstein. “Now they have to execute on that.”

Nipper, Ørsted’s chief executive, is optimistic, saying the “extreme” circumstances of the past few years are normalising. “Has it become more difficult than eight or 10 years ago? Absolutely,” he says, reflecting on the environment for offshore wind. “But is it a totally different proposition? No.”

Having already abandoned two big projects in the US and secured permits for another, Ørsted is — perhaps ironically — less exposed than some rivals to the policy disruptions of a second Trump term.

How much of a difference Trump and his proposed energy secretary, oil-industry boss Chris Wright, will make remains to be seen. Renewables grew during his first presidency, and Republican states have benefited from the Inflation Reduction Act he wants to halt. But plans to increase tariffs on imports could push up costs in the US.

Meanwhile, boosted by high fossil fuel prices, oil and gas producers have been rethinking their positions, with both Shell and BP diluting plans to diversify away from fossil fuels. The move has been criticised by campaigners, but many shareholders take a more nuanced view.

“There was a view a little while ago that [Ørsted’s path] was the path for all oil companies,” says Nazmeera Moola, sustainability director at Ninety One. “[But] we’ve increasingly come to the conclusion that’s a naive expectation — these are fundamentally different businesses.”

Yet Eldrup insists that Ørsted’s path was the right one, despite its challenges. “The world is changing and you have to change your business model,” he says. “What we often see is companies doing it too late. We managed to be in front of the curve.”

Neubert, the company’s former deputy CEO, agrees that renewables are still the way forward. “It’s much cheaper to save the world than to destroy it,” he says.

Additional reporting by Malcolm Moore

Data visualisation by Janina Conboye

#worlds #biggest #offshore #wind #company #blown