Cocoa market on the brink of big price surge

Unlock the Editor’s Digest for free

Roula Khalaf, Editor of the FT, selects her favourite stories in this weekly newsletter.

The writer is the founder and chief investment officer of Andurand Capital Management

The outlook for cocoa beans offers unwelcome tidings for chocolate makers hoping prices are on the retreat.

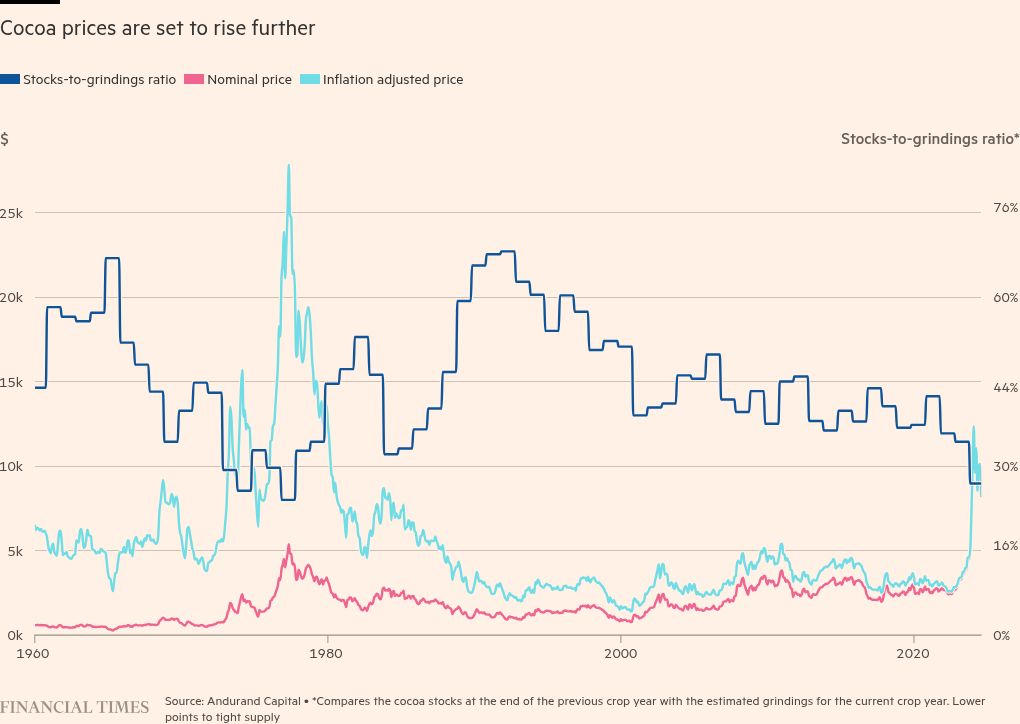

After an explosive rally in the first four months of the year, prices have cooled somewhat. Having started the year at about $4,400 per tonne, cocoa beans futures prices peaked at $12,000 in April — well above the inflation-adjusted decade average of $3,400. Yet by May, prices plummeted to $7,000 a tonne. But the respite is likely to be temporary. The prospect of a multiyear structural supply-demand deficit in cocoa beans will mean much higher prices are coming.

This is likely to catch out many chocolate makers that have been betting at their peril on a more sustained fall in prices, draining their stockpiles while reducing price hedges from eight to nine months of demand to five months. The strong pod count recorded from May to August had raised hopes among the makers that a rebound in production would replenish inventories, especially following the 500,000-tonne deficit in the 2023-24 season — the third consecutive annual shortfall and largest ever. This shortfall is attributed to a 13 per cent drop in global cocoa output due to much weaker production in Ivory Coast and Ghana — responsible for more than half of the world’s production.

Many pointed to the El Niño warming weather phenomenon as the primary driver of this poor harvest, expecting a transition to the cooling La Niña pattern to revive yields. However, recent data has dashed those hopes. Pod counts in key producing regions have deteriorated, and the 2024-25 season is now forecast to post a deficit of 160,000 to 200,000 tonnes, according to Forestero, a leading cocoa research company, and this time from a depleted inventory base.

Exchange-held stocks in Europe and the US have plunged from 400,000 tonnes in December 2023 to just over 100,000 tonnes — the lowest amount ever recorded. Such dwindling reserves amplify concerns about a prolonged supply squeeze. Yet the weather alone cannot shoulder all the blame. Structural issues are at the crux of the crisis. New deforestation laws have discouraged farmers from expanding plantations, while a global fertiliser shortage, exacerbated by Russia’s war in Ukraine, has led to lower usage rates. West Africa is also grappling with an ageing tree stock and the spread of the cocoa swollen shoot virus.

The virus has long been recognised as a production killer. Once symptoms appear, trees generally die within four years with yields significantly affected from the first year. A recent study by Forestero, using a new DNA-based technology developed by SwissDeCode, concluded that the current prevalence of CSSV in cocoa farms in West Africa is about 67 per cent, much higher than 30 per cent previously thought.

Assuming that most infected trees develop symptoms, this would suggest an impending collapse of production in Ivory Coast and Ghana. Cocoa expert and head of research at Tropical Research Services, Steve Wateridge, noted that Ivory Coast production could halve over time due to the spread of CSSV, in line with other disease-related production shocks.

The fragility of cocoa supply is underscored by its geographic constraints. Grown primarily within a narrow equatorial belt, cocoa is highly vulnerable to regional shocks. Historical precedents are sobering: Brazil’s output plummeted by 70 per cent within five years of the witches’ broom disease outbreak in 1989, and CSSV was a major cause of the 50 per cent decline in Ghana production in the 1970s. Should West Africa face a comparable crisis, the global market would struggle to offset the shortfall. Cocoa trees take roughly four years to mature, meaning any new planting initiatives would offer no immediate relief.

In some commodity markets, demand destruction through higher prices might close a supply gap. But demand for chocolate — and hence cocoa beans — is relatively inelastic. Even if you take, for example, an avid chocolate eater who consumes 50g of 70 per cent cocoa dark chocolate a day, they would pay cocoa costs of just 35 cents per day. A doubling in prices is unlikely to deter their consumption.

Similar levels of inventories-to-demand ratio led to an inflation adjusted peak of $28,000 a tonne in 1977 after a five-year bull run. With the current rally barely a year old and supply headwinds likely to worsen for at least four years, the stage appears set for cocoa prices to reach new inflation-adjusted highs.

Andurand Capital holds investment positions in the cocoa market

#Cocoa #market #brink #big #price #surge