Rio Tinto won’t easily ditch its dual structure, despite its lack of style

Unlock the Editor’s Digest for free

Roula Khalaf, Editor of the FT, selects her favourite stories in this weekly newsletter.

Even when a style goes firmly out of fashion, some loyal devotees still don’t give it up. Take Kate Moss and skinny jeans.

The corporate world’s equivalent is the dual-listed company (DLC) structure. Typically this is where two companies have — instead of a conventional merger — kept their separate legal identities and stock market listings but are operated as a single business.

Benefits can include tax advantages. But increasingly DLCs are seen as outmoded, value destructive and a potential block to large M&A. Well-known DLCs have been collapsed in recent years, including BHP, Shell and Unilever — often under pressure from activist investors.

Rio Tinto, a nearly three decade-long DLC devotee, is under fire from activist fund Palliser Capital to follow suit by unifying its corporate structure in Australia and shifting its primary listing to Sydney.

Palliser this week upped a campaign it began in May, claiming Rio’s complex structure had been an “unmitigated failure”.

Parts of Palliser’s argument are compelling. Most DLCs came into being decades ago. Its difficult to see companies making the same choice today.

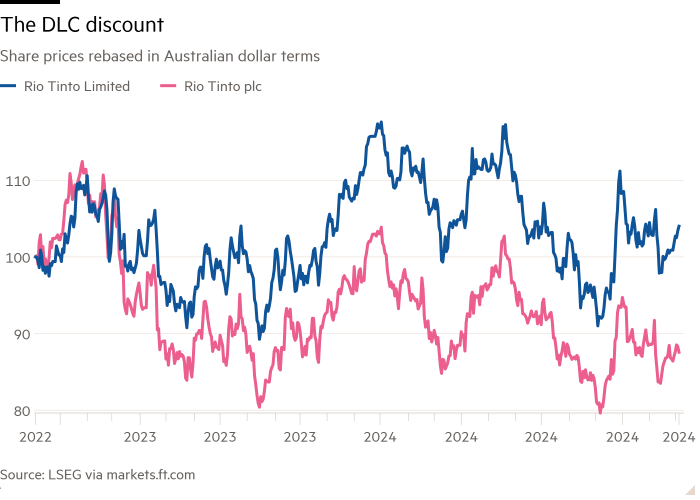

Rio’s London-listed shares trade at a big discount to those of Sydney-listed Rio Tinto Limited — about 19 per cent. This could complicate any mining megadeals, given these are generally all-share affairs. Technically stock-based acquisitions should be possible with DLC structures — indeed BHP tried to pull one off through its failed 2008 bid for Rio. But Palliser claims Rio’s near exclusive use of cash for M&A highlights the complexity of doing so in reality.

This is an old debate. And Rio’s chief executive Jakob Stausholm says he has considered the merits of simplifying. But the company and its advisers came up with different answers on several key points. In particular, the tax costs. Rio claims these would amount to “mid-single-digit billions of dollars”; Palliser insists they would be closer to $400mn. There is also disagreement over the level at which the shares of a unified company would trade.

This has echoes of the fight between rival miner BHP and activist Elliott Advisors when the latter campaigned for BHP to dump its DLC structure. BHP was always more Aussie than British anyway. And boss Mike Henry was more motivated to invest time and money in gearing up the company for a return to big dealmaking.

So far, Rio is living up to its more conservative reputation. Its biggest deal since 2007 is its recent $6.7bn swoop for Arcadium Lithium. In the summer, Stausholm warned of the “big risk” associated with mega M&A.

This won’t be the last of anti-DLC campaigning. But it will take more than peer pressure to make Rio ditch this well-worn style.

#Rio #Tinto #wont #easily #ditch #dual #structure #lack #style