Trade war fallout could trigger deep Eurozone rate cuts, Pimco warns

Unlock the Editor’s Digest for free

Roula Khalaf, Editor of the FT, selects her favourite stories in this weekly newsletter.

Bond giant Pimco has warned the fallout from a trade war launched by Donald Trump could drive Eurozone interest rates back down towards “emergency levels” as policymakers seek to soften the blow on the bloc’s struggling economy.

Andrew Balls, chief investment officer for global fixed income at the $2tn-in-assets manager, said he expected there to be “multiple rounds of the game” when it comes to tariffs, a policy repeatedly threatened by the US president-elect.

“The worst version of the trade situation would be difficult” for Europe, Balls told the Financial Times. “I tend to think that we’re pricing in a fairly benign path.”

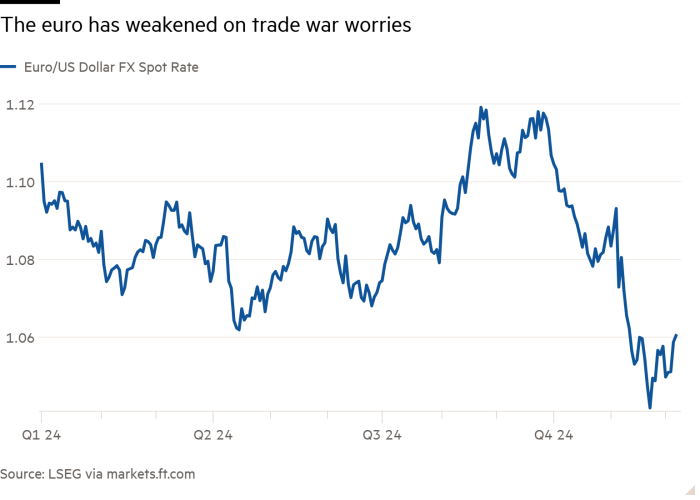

European assets have been big losers as markets brace for Trump’s “America First” policy package. The euro is down more than 5 per cent since late September to around $1.06 as investors shift to expect more aggressive rate cuts from the European Central Bank as it offsets a dimmer outlook for the region’s exporters.

Traders in swaps markets are now betting that the ECB’s deposit rate will fall as far as 1.75 per cent, from the current level of 3.25 per cent, before the central bank stops cutting.

But Balls thinks the ECB could go further. “I imagine you could easily price in lower terminal rates, in the event of worse-than-expected outcomes where the ECB is going to more emergency levels of policy rates,” he said. As a result, Pimco expects the euro to fall further against the dollar.

Two years ago, the ECB ended eight years of negative interest rates as it battled the burst of inflation that followed the Covid pandemic.

Some investors have viewed Trump’s nominee for Treasury secretary, hedge fund manager Scott Bessent, as a moderating influence on Trump’s more radical economic policies. That belief has sparked a retreat in the dollar from its post-election high.

“I think markets are broadly pricing in quite optimistic outcomes,” Balls said. “You can see upside risks [but] it’s easier to see downside risks.”

In the UK, a hit to the economy from a global trade war would also leave “plenty of room” for lower so-called terminal interest rates, Balls said.

Currently, investors are expecting three quarter-point cuts from the Bank of England by the end of next year, taking UK rates to 4 per cent.

Pimco currently favours UK gilts relative to US Treasuries on the view that rates could fall further, he said.

Despite his gloomy view on the risks facing the Eurozone economy, Balls said he does not expect further weakness in French government debt, which has been rocked by a recent budget crisis that led to the collapse of Michel Barnier’s government.

French 10-year borrowing costs recently hit a 12-year high relative to those of Germany. Balls said the wider gap was a fair reflection of the poorer outlook for France’s public finances.

He also said that the lack of “contagion” in other Eurozone markets showed that the French crisis was unlikely to become a systemic issue for the currency bloc.

“We’ve had war, we’ve had [the] pandemic, we’ve had a whole set of shocks, [a] radical government in Italy, political trauma in France and a whole set of stress tests, and European markets have performed very well,” Balls said.

#Trade #war #fallout #trigger #deep #Eurozone #rate #cuts #Pimco #warns