BP and Shell rein in electricity ambitions to escape ‘valley of death’

BP and Shell spent a combined $18bn over five years to become major players in electricity. Now the oil majors are scaling back their ambitions in power generation after poor progress and widespread scepticism.

In 2019, Shell set a goal of becoming the world’s largest electricity company, with Maarten Wetselaar, director of gas and new energies at the time, forecasting that power revenues would equal those from oil and gas by the 2030s.

BP set out its own bold transition plan the following year under then chief executive Bernard Looney, promising to raise green energy spending tenfold to $5bn annually by 2030 and expand its renewable power generation business by 20 times in the same timeframe to about 50GW of capacity.

Both companies shrugged off questions over whether they had a competitive advantage in renewable energy. “We build and operate some of the biggest projects in the world,” Looney told the Financial Times in 2020. “I wouldn’t underestimate just how relevant some of those skills are.”

The two men have moved on, and after a few years of heavy spending, BP and Shell’s current management teams have conceded they may not possess such an advantage, or a deep enough balance sheet, to meet some of their hopes for renewable electricity.

Meanwhile BP’s share price is down more than 16 per cent this year, with Shell nearly 2 per cent lower. One energy chief executive remarked that the companies were caught in the “valley of death” between their traditional pro-fossil fuel shareholders and a new set of pro-climate investors.

Shell, which has invested roughly $11.8bn on its power business since 2019, according to research group Accela, has sold its electricity retail business in the UK, the Netherlands and Germany, withdrawn from the Chinese electricity market and told its staff last week it would not seek out any new offshore wind projects.

BP, which Accela estimated to have spent $6.8bn on low carbon power, this week said it had placed its offshore wind assets in a joint venture with Japanese partner Jera, allowing it to halve its expected capital expenditure on offshore wind by the end of the decade and move any future debt off its balance sheet.

Analysts expect it to drop or scale back its target for 50GW of renewable capacity by 2030 at its capital markets day in February. Rohan Bowater, an Accela analyst, said its $3bn-$5bn target for renewable spending next year was also under threat.

Both BP and Shell are, so far, still committed to their solar, electric vehicle charging and power trading businesses. At the same time as pulling back from offshore wind, Shell said it had split its power division into two units, one focused on generation and the other on trading.

Alon Carmel, head of offshore wind at PA Consulting, said the pullback in the sector followed some “bold bets” from oil companies in areas “where the risks have turned out to be greater than perceived”. In particular, BP paid a high price to lease a swath of seabed off the German coast, while both companies have projects in the US, where Donald Trump’s incoming administration has signalled its opposition to offshore wind.

A senior energy investment banker also noted the hubris that permeated the offshore wind industry, which has been hit by higher interest rates and inflation in its supply chain.

“They wrongly got into a mindset of saying [they would not face] cost inflation in our supply chain, there’s not going to be cyclicality and the government’s always going to be supporting and underwriting us. All three of those have come home to roost in a negative way,” said the investment banker.

The oil majors are unlikely to be missed by the wider industry.

“They had a negative impact,” said Jérôme Guillet, managing director at Snow, a renewable energy advisory boutique, saying they lacked the cost discipline of utilities and smaller developers, overpaid for assets and tried to squeeze the supply chain in an effort to succeed.

“Then they complained loudly that the economics did not work and gave the sector a bad name.”

Other European oil companies are also rethinking their plans. Equinor, Norway’s state oil and gas company, has slowed its buildout of renewables and instead bought a stake in Danish wind power specialist Ørsted. Analysts at RBC Capital Markets suggested that this may be a less capital intensive path to decarbonisation in the medium term.

Italy’s Eni has combined low-carbon growth businesses such as biofuels with cash-generating units such as service stations, and sold stakes in the spin-offs. KKR, the private equity firm, bought a quarter of its Enilive division at a $13bn valuation.

The changing strategies reflect the challenge for listed oil companies to steer a path through the energy transition, with the company chief saying it would be “very hard, almost impossible” for them to transform.

“These companies are owned by investors who like to own fossil fuel companies, and if they were 50 per cent green they’d be owned by a totally different group of shareholders. There’s almost no overlap” he explained.

He continued: “Your current shareholders will sell when you get to 20 per cent green, but the new shareholders will not buy until you are 50 per cent green. So there’s a valley of death in between.”

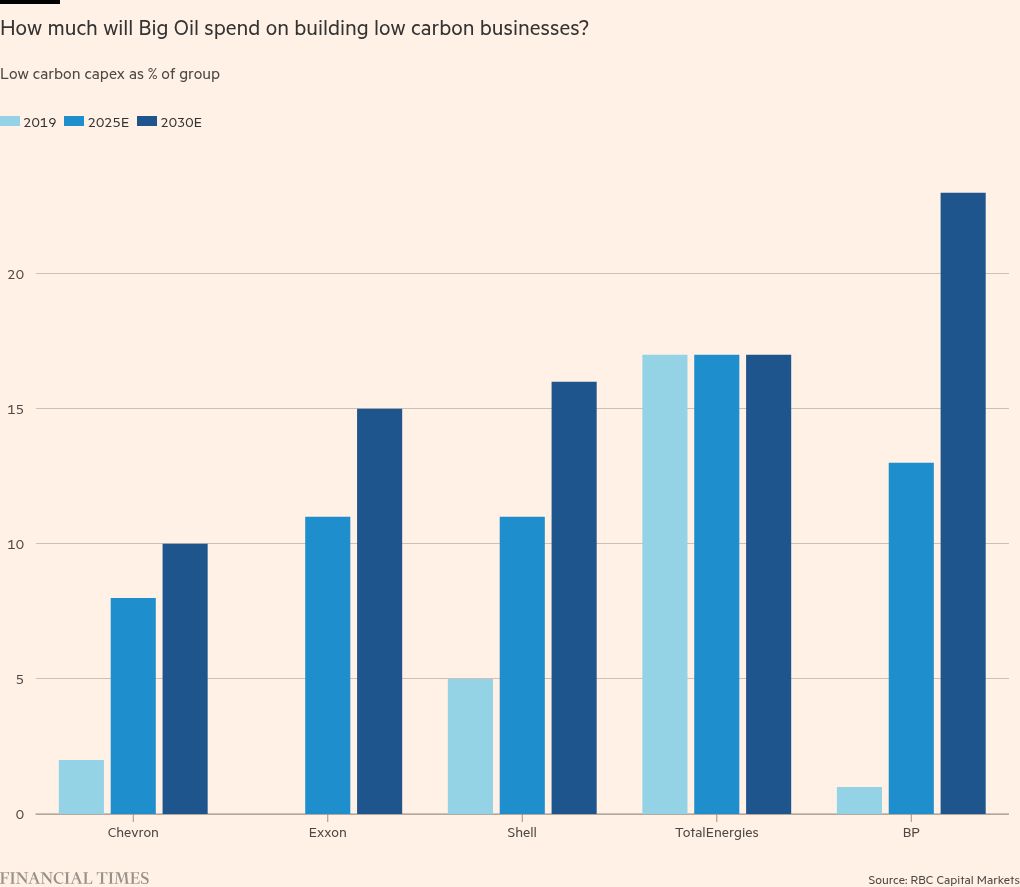

In Europe, only TotalEnergies has shown success in bridging the gap. Moody’s this week upgraded the French company’s credit rating, noting the “improved quality” of its business, after TotalEnergies cut the cost of its oil production and built a power business that included 14.5GW of renewables.

Meanwhile, almost all other oil companies have slowed spending on low carbon. RBC Capital Markets said that across its basket of nine US and European oil companies, low carbon spending fell to 10 per cent of capital expenditure in 2024, “well below what expectations may have been a few years ago”. It estimated that low carbon businesses will account for 7 per cent of BP’s earnings by 2030, falling to 5 per cent at Shell.

The energy investment banker said that while Shell had pulled back firmly from electricity businesses such as offshore wind, BP’s move suggested it was still trying to find a way forward with its plans, but preferably off its debt-heavy balance sheet and with external partners.

“Shell is saying it’s probably going to do less, while BP is going to try to do the same but with a certain capital frame,” they said.

“They’re looking to find someone to share the valley of death with,” they added. “And when they come out of the other side, they hopefully have a chunk of cash flow at the end of the decade.”

Climate Capital

Where climate change meets business, markets and politics. Explore the FT’s coverage here.

Are you curious about the FT’s environmental sustainability commitments? Find out more about our science-based targets here

#Shell #rein #electricity #ambitions #escape #valley #death