Defence bounty eludes the UK’s Chemring

Unlock the Editor’s Digest for free

Roula Khalaf, Editor of the FT, selects her favourite stories in this weekly newsletter.

Raging wars and ramped up defence budgets are swelling the sector’s order books. British defence specialist Chemring is no exception, with a record £1.04bn of orders on the slate. But there the similarities to the wider industry start to taper.

A smaller share of Chemring’s revenues are dropping through to the bottom line — its operating profit margin shrank 70 basis points in the year to end-October, to 13.9 per cent. That is in sharp contrast to peers, which are busily juicing more out of every dollar of revenues.

The FTSE 250 constituent can claim some bad luck. It has pinned its woes on tried-and-tested canards: bad weather and legacy business. The former shuttered a Tennessee plant that makes infrared devices to counter enemy attacks. Add in faltering efforts to automate processes and the factory is expected to continue running on partial capacity this year.

US contracts to supply countermeasures, awarded in 2016, were taken on at low margins and — apparently — longer than anticipated timeframes. Chemring thought they would be out the door last year; instead they will weigh on group margins through this year too.

That explains why it has issued somewhat guarded guidance. Chemring expects another year similarly weighted towards the second half and is focused on “appropriate margins, mindful of financial constraints from our customers”.

Longer term, it is targeting about £1bn of revenues by 2030, getting on for double last year’s £510.4mn. That implies compound annual growth of almost 12 per cent, ahead of both last year and of the previous five years’ run rate.

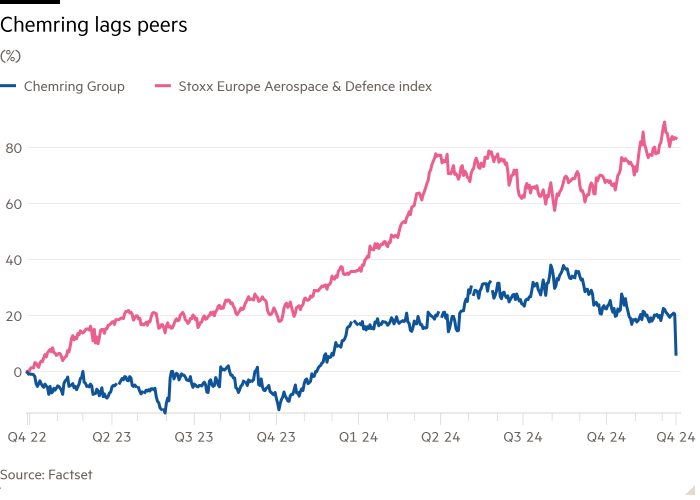

Still, the demand backdrop remains propitious. Nato member states, with the US as a probable exception, are all committed to spending more on defence and, specifically, disbursing more of that largesse within Europe. With exposure to both traditional and digital weaponry, Chemring should by rights be a beneficiary. But its track record engenders wariness. Shares, down 11 per cent after reporting results on Tuesday, are up by only a quarter since Russia invaded Ukraine in early 2022. Over the same period, the Europe aerospace and defence sector sub index has roughly doubled.

Yet Chemring’s shares still trade on a forward price/earnings multiple of 18 times, on S&P Capital IQ numbers, ahead of bigger compatriot BAE Systems. Few are in any doubt that this is a company in the right time and place. Now it just needs to ensure it has the capacity and wherewithal to take advantage.

#Defence #bounty #eludes #UKs #Chemring