Self-employed workers struggle to bridge gap in retirement savings

Self-employed workers, even in some of the world’s biggest economies, are struggling to build up the savings they need to fund the lifestyles they seek in retirement, according to the latest data.

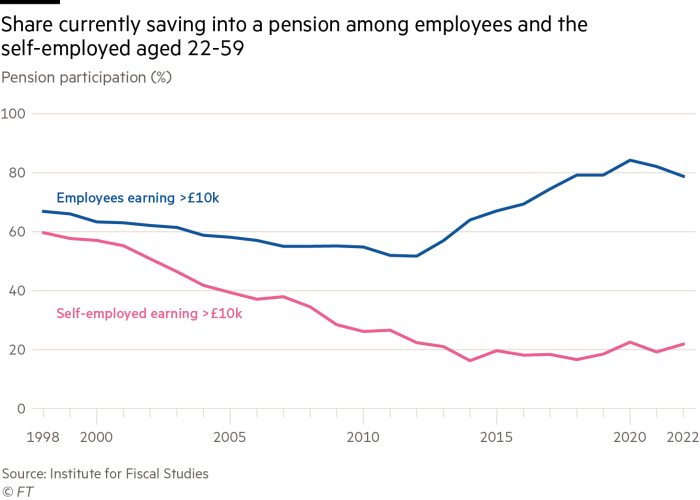

In the UK, a declining level of pension contributions from self-employed workers contrasts starkly with an accelerated push for employees to be auto-enrolled in pension schemes by their employers.

One in five self-employed workers earning more than £10,000 a year put money into a pension in 2022. But that figure is unchanged since the early 2010s, and has dropped from three in five 26 years ago, researchers at the UK’s Institute for Fiscal Studies have found.

By contrast, the IFS reports that 80 per cent of employees on a similar salary paid into a workplace pension scheme in 2022. Companies, since the introduction of auto-enrolment in 2012, must enrol eligible staff into a pension scheme unless the worker actively opts out.

This UK system, which puts the onus on the self-employed worker to arrange their own pension plans and offers no government assistance, is “no longer fit for purpose”, the IFS concludes in its September pensions review.

Policymakers believe the issue is worth highlighting as the self-employed made up 13 per cent of the total UK workforce in the second quarter of this year, and 15 per cent a decade ago, according to latest figures from the Office for National Statistics.

A critical part of solving this problem is understanding the wide range of financial profiles within the self-employed sector, argues Rachel Vahey, head of public policy at AJ Bell, the UK investment platform. It is “not a distinct cohort”, she says.

A report by the Centre for Research on Self-Employment in partnership with the Institute for Employment Studies outlines nine distinct categories of self-employed people, from “low pay, dependent and insecure” to “high pay, independent and secure”.

As a result, it can be hard to gain an accurate picture of the state of savings among some self-employed people. Many have assets other than pensions that they plan to use in retirement. For instance, some intend to sell their business or move to a smaller home.

Others, however, do not have this level of forward planning or wealth — and are neglecting to plan effectively for retirement. “[This] leaves them looking at a retirement where they are dependent on the state pension [as] the only savings behind them,” says Vahey.

However, the UK is not the only country to face these issues. Larry Fink, chief executive of BlackRock, the world’s biggest investment manager, in his annual letter to investors, highlighted the 57mn Americans without access to retirement plans at work. Many of these are self-employed.

One of the biggest barriers stopping self-employed people from saving into a pension is the unpredictability of when they will be paid and the financial uncertainty that creates. “We have got to do more in getting people to pay self-employed [workers] quicker,” says Renny Biggins, head of retirement at The Investing and Saving Alliance, a financial services industry group.

The nature of self-employment can also make saving regularly difficult. “If you put money into a pension in your 20s, you can’t touch it for the best part of 40 years,” says Biggins. “How is that really going to help a self-employed person?” he asks — especially if they need the money or fear their business will go under.

Even for those in the UK who can afford to save into a pension, navigating the complex system of personal pensions and tax breaks is challenging. Just 9 per cent of UK consumers have paid for financial advice in the past two years, compared with 11 per cent in 2023, according to a report published in July by The Lang Cat, an industry consultancy.

Professional advice, which must adhere to strict regulations, is often expensive, running into thousands of pounds over a few years for several consultations. General financial coaching, however, can bring the costs down.

In order to bridge this gap, the UK’s Financial Conduct Authority has proposed an option that would allow authorised companies, such as product providers, to guide customers towards certain schemes based on what others in a similar position find suitable. Since this “targeted support” would not count as regulated financial advice, it would be cheaper and easier to provide — lowering the entry bar for consumers to take up and act on retirement planning guidance.

Another suggestion to help the self-employed is the development of “sidecar savings” schemes. A sidecar account is an instant access savings account that is tied to a pension, which would allow account holders to access savings in case of an emergency.

“The idea is that, alongside the illiquid pension saving, you have a short-term savings vehicle, like an emergency fund, that is in an accessible savings pot,” explains Robin Armer, a director at Nest, the state-backed UK workplace pension fund. “That gives them some protection against the impact of a financial shock that might stop them from persisting with their long-term savings.”

Ultimately, though, regulation is required to push people into saving properly, Armer believes, and it must reflect the inconsistent levels of wealth within the cohort of self-employed people in the UK.

AJ Bell’s Vahey agrees. “This is not a one-size-fits-all situation,” she says.

#Selfemployed #workers #struggle #bridge #gap #retirement #savings