Financial markets do not trust the BoE to deliver low inflation

This article is an on-site version of our Chris Giles on Central Banks newsletter. Premium subscribers can sign up here to get the newsletter delivered every Tuesday. Standard subscribers can upgrade to Premium here, or explore all FT newsletters

On one level, the Bank of England has had a remarkably good inflation crisis. A year ago, the UK’s central bank expected inflation still to be above 3 per cent in the final quarter of this year, interest rates still to be above 5 per cent and unemployment pushing ever closer to 5 per cent.

The reality shows inflation hovering around the BoE’s 2 per cent target, interest rates falling faster to 4.75 per cent in November and the official measure of unemployment at 4.3 per cent.

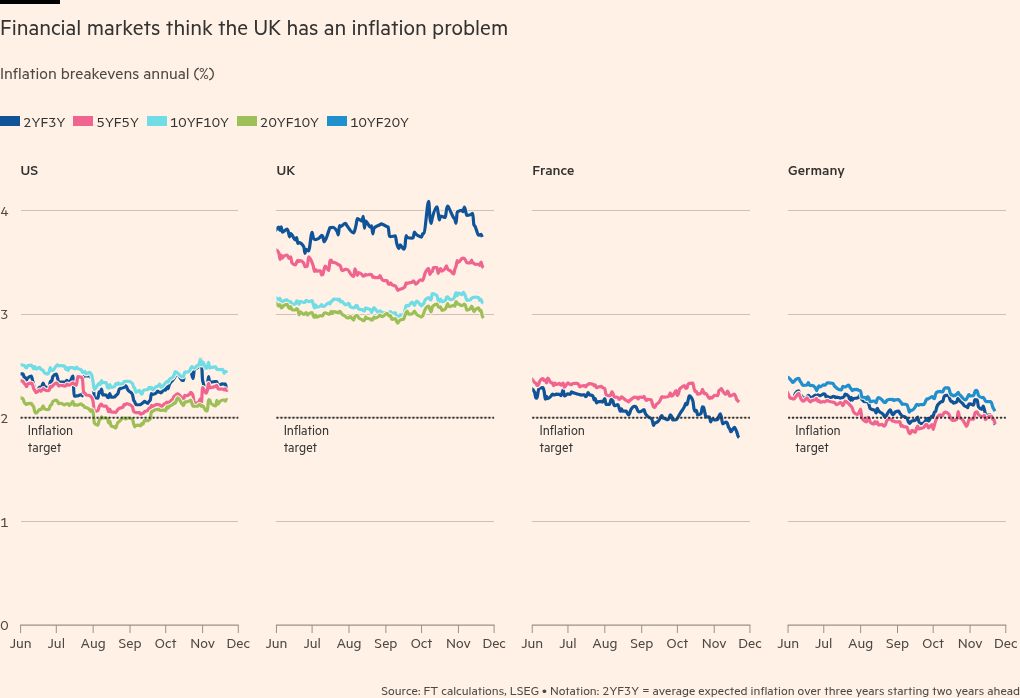

Financial markets do not buy the good news story, however. They are demanding an inflation risk premium for the UK, which they do not for the US, France or Germany. Derived from the nominal and real returns of UK government bonds, it is relatively straightforward to calculate break-even rates of inflation, representing financial market expectations of inflation over different time periods.

These are shown in the chart below for the UK, US, France and Germany. In the short term, the market expectation of UK inflation over the three years two years from now (ie between late 2026 and late 2029) is close to 4 per cent, while very long-term market expectations hover around 3 per cent.

This contrasts with market expectations of French and German inflation, which are extremely close to the European Central Bank’s 2 per cent inflation target. Those in the US are a little higher, but the market rates are based on US CPI inflation, while the Fed targets PCE inflation. With CPI averaging 0.36 percentage points higher than PCE since the start of 2010, US market inflation expectations are also in line with the Fed’s target.

The UK’s exceptional status here has been a long-standing phenomenon and, in the past, there has been a straightforward explanation.

The UK’s market inflation estimates are based on the retail prices index, which has averaged 1.1 percentage points above the CPI inflation measure targeted by the BoE. Remove that amount from the UK’s market expectations, especially for long-term indicators and the UK’s market expectations fall back to the BoE’s 2 per cent target.

But that is no longer a valid adjustment to make because from February 2030, the calculation of the RPI will change to be identical to a third inflation measure, CPIH. This measure is largely the same as CPI, but includes housing costs of owner-occupiers using the concept of owners equivalent rent. It is methodologically close to the US CPI in that respect.

After a long struggle to remove well known problems with the RPI and with all legal challenges exhausted, there is no doubt that the RPI will change to be CPIH from February 2030 and that “inflation protection” in UK index-linked government bonds will fall considerably. (I put inflation protection in inverted commas because the protection was previously too high to compensate for inflation). I will not go into the reasons why this is not remotely an expropriation or a disguised default, but you can read some of the gory details here.

Although CPIH is currently elevated due to rental inflation being high, we would expect the inflation protection in UK index-linked bonds to fall by about 1 percentage point in the 2030s as you can see from the chart.

There is therefore an important question about financial market expectations of UK inflation. In the year before and after the new methodology, inflation swaps market pricing shows that expected RPI inflation falls just over 0.4 percentage points. The change in inflation calculation methodology is being priced in, but not fully.

As the chart below shows, well after the change in 2030, financial markets expect UK CPIH inflation to be a little over 3 per cent while the BoE’s inflation target is 2 per cent.

The pink line represents the BoE’s own estimate of inflation expectations at all points in the future, derived from the same nominal and index-linked government bond markets. It is heavily smoothed so cannot accurately pick up the change in the RPI calculation methodology.

There are only so many explanations for this market pricing that can exist. They are not mutually exclusive.

-

Financial markets believe the RPI methodology change will not happen. I think this is incorrect given the public position of the UK Statistics Authority

-

The real yield on UK index-linked gilts is artificially depressed by high demand for these bonds from pension funds, thereby raising the implied expected inflation component. If this is the case, Sushil Wadhwani made a strong case for the government to issue more index-linked government bonds. If financial markets expect 3 per cent inflation and the BoE will deliver 2 per cent inflation, these will make government borrowing much cheaper than nominal bonds. The UK government’s policy is to do the opposite of this. It is potentially costly

-

Financial markets do not find the BoE’s 2 per cent inflation target credible and believe the BoE will achieve a figure closer to 3 per cent for CPIH. As the table above shows, the past suggests this would not be an entirely unreasonable assumption. Even after the recent inflation, long-term average inflation for the US and Eurozone are only a touch over 2 per cent

-

Financial market pricing is wrong. Hey, markets are not always efficient

BoE credibility

Clare Lombardelli, the BoE’s deputy governor for monetary policy, sought to address any issues about the central bank’s credibility, forecasting and policy with a speech yesterday at the annual BoE watchers’ conference.

Although it was very much a work in progress, Lombardelli said the bank was working on its models, that the changes in forecasting practices would be large and that they were only just starting.

She was notably hawkish, saying that in her view although the upside and downside risks were similarly sized, she thought outcomes would be worse if inflation remained too high for longer so gave that risk greater weight. Her colleague on the MPC, Swati Dhingra, shared much of the analysis but weighted risks differently.

But all noises from the BoE suggest it is minded to withdraw restrictiveness gradually (which means at a roughly quarterly pace) until there is more evidence on the persistence of inflation one way or the other. That financial markets (unlike households) do not trust policymakers is not raised in most polite conversations.

What I’ve been reading and watching

-

Ian Harnett, chief investment strategist at Absolute Strategy Research, argues that central banks should seek to rectify inflation overshoots with a period of below target price rises

-

Former UK Monetary Policy Committee member DeAnne Julius thinks everything above here is too rosy and the UK is heading for stagflation

-

US finance and business breathes a sign of relief with the pick of Scott Bessent as Trump’s Treasury secretary

-

Europe needs to save less, says Martin Sandbu, and he comes up with a raft of policy ideas to achieve it, many of which are hated by the European economic establishment

A chart that matters

Over the past month and since Donald Trump became president-elect, expectations of US interest rate cuts have weakened significantly and the market-implied path of interest rates is now much higher than the start of the year. This reflects a combination of expectations of looser fiscal policy, a view that neutral rates are higher and that policy is not as restrictive as thought and a couple of slightly disappointing months of inflation data.

UK expectations have followed the Fed, despite BoE forecasts suggesting inflation would be broadly on target with interest rates falling well into numbers beginning with a three. The UK Budget’s fiscal loosening and some inability of UK markets to divorce themselves from the Fed are thought to be to blame. In contrast, European market interest rate expectations have not budged over the past month.

Recommended newsletters for you

Free lunch — Your guide to the global economic policy debate. Sign up here

Trade Secrets — A must-read on the changing face of international trade and globalisation. Sign up here

#Financial #markets #trust #BoE #deliver #inflation