Gilt investors urge Reeves to keep investment ambitions in check

Unlock the Editor’s Digest for free

Roula Khalaf, Editor of the FT, selects her favourite stories in this weekly newsletter.

Chancellor Rachel Reeves’s ambitions to borrow billions more for investment are set to bump up against tight constraints in the bond market as investors warn they have a limited appetite for fresh UK debt.

Asset managers have said the chancellor needs to tread carefully as she seeks to overhaul the UK fiscal regime ahead of the Budget on October 30, with some highlighting the risks if the Treasury adopts a revised debt target that boosts borrowing capacity by tens of billions of pounds.

Some gilt investors say they are wary of extra borrowing that goes beyond £10bn to £20bn.

“Anything higher than this could push gilts over the edge,” said Craig Inches, head of rates and cash at Royal London Asset Management. The market is “fearful ahead of the upcoming Budget borrowing figures”.

Reeves said at the Labour party conference that she wanted the Treasury to be better at counting the benefits of investment and not just the costs, in words that raised expectations of tweaks to government debt rules that are currently hemming in capital spending.

A series of options are under discussion within the Treasury.

One route would involve Reeves easing headline debt figures by removing liabilities associated with government “policy banks” such as the UK Infrastructure Bank, the new National Wealth Fund and new state-owned company GB Energy.

Research from the London School of Economics this summer suggested this could create additional public investment capacity totalling around £18bn over the remainder of the decade.

“While some see this as an ‘accounting trick’, the UK is currently an outlier by including such debt as part of the government balance sheet,” said Ales Koutny, head of international rates at Vanguard.

Alternatively, the Treasury could adjust its debt rule to better account for assets, as well as liabilities, on the public books.

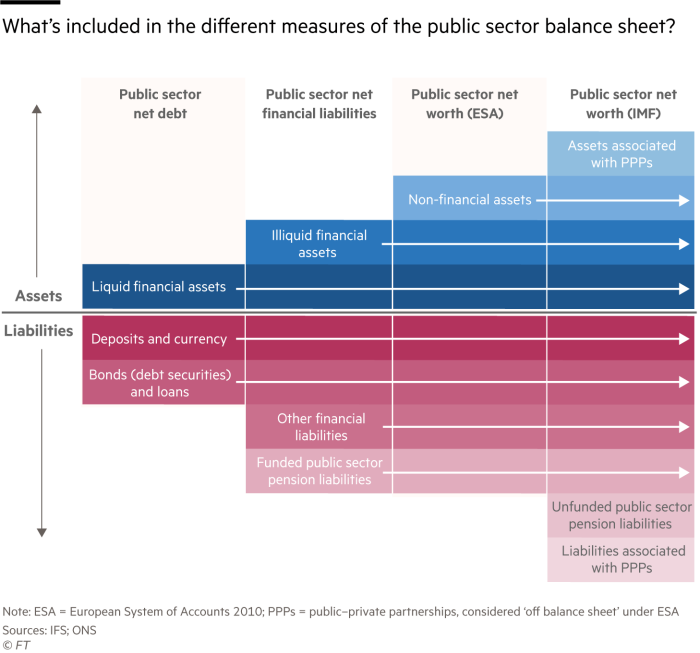

As things stand, public sector net debt only counts highly liquid assets like cash as an offset to the national debt.

An alternative measure, called public sector net financial liabilities (PSNFL), captures equity and debt investments such as those made by government vehicles such as the Infrastructure Bank, bolstering the UK’s fiscal room for manoeuvre.

The IMF has urged countries to consider a different balance sheet measure called public sector net worth (PSNW), which also counts assets as well as liabilities, but this includes hard-to-value projects such as hospitals and schools.

Shifting the debt target to PSNFL risks upsetting markets if it is not handled carefully, economists said, given it would boost budget headroom against the debt rule to more than £60bn based on the March forecast, from just £9bn.

“If they shift to PSNFL, they would need to be very clear they would not use all that extra headroom it creates,” said Tom Pope at the Institute for Government think-tank.

“They may decide that pulling the policy banks off the public balance sheet instead achieves their goal of creating space for some additional growth-enhancing investment without looking so radical.”

Shamil Gohil, fixed income portfolio manager at Fidelity International, said the markets were comfortable with Labour’s existing plans to shift the deficit rule to one that targets the current budget, stripping out investment.

But he said there was “growing concern” over potential changes to the parallel debt rule.

“The UK is in a predicament — the rules are too constraining to allow for much-needed investment but not constraining enough to ensure long term debt sustainability,” he added.

Any extra borrowing for investment would have a knock-on impact on the current budget rule, given it would entail extra interest costs which add to day-to-day spending. This will constrain the government’s ability to borrow more for investment.

As of the government’s March forecasts the headroom against the current budget was just £14bn.

New economic and fiscal forecasts delivered by the Office for Budget Responsibility, the UK fiscal watchdog, to the Treasury last week are not expected to provide much of a boost for the chancellor.

However the Treasury has already been contemplating a change to its net debt target to minimise the impact of losses by the Bank of England on its quantitative tightening scheme, a move that would hand the government up to £16bn of extra headroom against its debt rule.

The sale of UK government debt was met with relatively weak demand this week, which “points to a nervous investor base ahead of an uncertain October Budget”, said Gohil.

Still, most investors expect the Treasury to tread carefully with its borrowing plans.

“We anticipate a cautious approach from the government,” said Peder Beck-Friis, economist at bond fund giant Pimco, who finds gilts “attractive” at current levels.

He added that “the priority seems to be a continued reduction in the deficit . . . fiscal policy will probably remain tight in the coming years”.

A Treasury spokesperson said the Budget would be built on “robust fiscal rules that were set out in the manifesto”.

“These include moving the current budget into balance so that day-to-day costs are met by revenues, and debt falling as a share of the economy by the fifth year,” they added.

#Gilt #investors #urge #Reeves #investment #ambitions #check