Is a repeat of the 2019 repo crisis brewing?

Unlock the Editor’s Digest for free

Roula Khalaf, Editor of the FT, selects her favourite stories in this weekly newsletter.

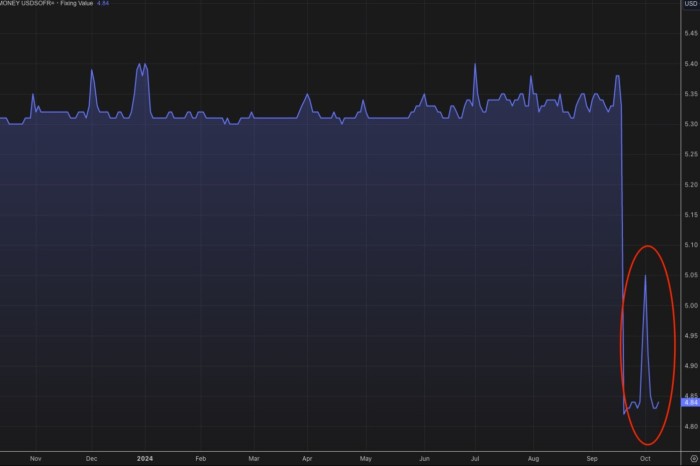

At the end of September there was a big spike in the Secured Overnight Financing Rate. This may already be putting you to sleep but it’s potentially a big deal, so please stick around.

SOFR was created to replace Libor (R.I.P.). It measures the cost of borrowing cash overnight, collateralised with US Treasuries, using actual transactions as opposed to Libor’s more manipulation-prone vibes. You can think of it as a proxy of how tight money is at any given time.

Here you can see how SOFR generally traded around the central point of the Federal Reserve’s interest rate corridor, and fell when the Fed cut rates by 50 basis points in September. But on the last day of the month, it suddenly spiked.

This is natural, to an extent. There’s often a bit of money tightness around the end of the quarters, and especially the end of the year, as banks are keen to look as lean as possible heading into reporting dates. So SOFR (and other measures of funding costs) will often spike a little around then.

But this was FAR bigger than normal. Here is the same chart but showing the end-of-2023 spike, and little dimples at the end of the first and second quarters.

Indeed, Bank of America’s Mark Cabana estimates that this was the single-biggest SOFR spike since Covid-19 wracked markets in early 2020, and points out it happened on record trading volumes.

Cabana says he was initially too hasty in dismissing the spike as driven by a short-term collateral shortage and unusually large amounts of window-dressing by banks. In a note published yesterday, he admits to overlooking something potentially more ominous: reserves seeping out of the banking system.

We have long believed funding markets are determined by 3 key fundamentals: cash, collateral, & dealer sheet capacity. We attributed last week’s funding spike to the latter 2 factors. We overlooked extent of cash drain in contributing to the pressure.

The increased sensitivity of cash to SOFR hints of LCLOR.

LCLOR stands for “lowest comfortable level of reserves”, and might require a bit more explanation.

Back in ye olde times (pre 2008), the Fed set rates by managing the amount of reserves sloshing around the US monetary system. But since 2008 that has been impossible due to the amount of money pumped in through various quantitative easing programmes. That has forced the Fed to use new tools — like interest on overnight reserves — to manage rates in what economists call the “abundant reserve regime”.

But the Fed has now been engaging in reverse-QE — or “quantitative tightening” — by shrinking its balance sheet sharply since 2022.

The goal is not to get the balance sheet back to pre-2008 levels. The US economy and financial system is far larger than it was then, and the new monetary tools have worked well.

The Fed just wants to get from an “abundant” reserve regime to an “ample” or “comfortable” one. The problem is that no one really knows exactly when that happens.

As Cabana writes (with FT Alphaville’s emphasis in bold below):

Like the macro neutral rate, LCLOR is only observed near to or after it is reached. We have long believed LCLOR is around $3-3.25tn given (1) bank willingness to compete for large time deposits (2) reserve / GDP metrics. Recent funding vol supports this.

A similar dynamic was seen in ‘19. At that time, the correlation of changes in reserves to SOFR-IORB turned similarly negative. The sensitivity of SOFR to reserves correlation signalled nearing LCLOR. We sense a similar dynamic is present today.

Unfortunately, when reserve levels drop to uncomfortable levels, we tend to find out very quickly, in unpleasant ways.

Cabana’s mention of 2019 is a reference to a repo market crisis in September that year, when the Fed missed growing hints of tightness in money markets. Eventually it forced the Federal Reserve to inject billions of dollars back into the system to prevent a broader calamity. MainFT wrote a superb explainer of the event, which you can read here.

In other words, the recent SOFR spike could be a hint that we are approaching or already in uncomfortable reserve levels, which could cause a repeat of the September 2019 repo ructions if the Fed doesn’t act preemptively to soothe stresses.

Here are Cabana’s conclusions (his emphasis):

Repo is heart of markets. EKG measures heart rate & rhythm. Repo EKG flags shift. Cash drain has supported spike in repo. Fed should take repo pulse & sense shift. If Fed too late to diagnose, ‘19 repeat. Bottom line: stay short spreads w/Fed behind on diagnosis.

#repeat #repo #crisis #brewing