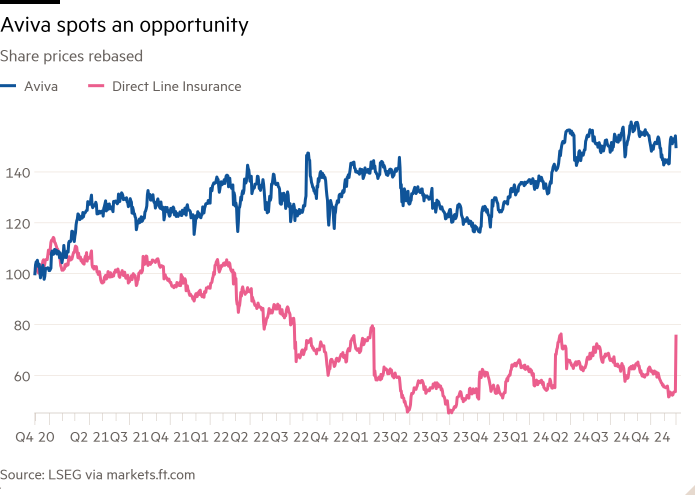

Direct Line playing hardball with Aviva bid

Unlock the Editor’s Digest for free

Roula Khalaf, Editor of the FT, selects her favourite stories in this weekly newsletter.

Can an offer at a near-60 per cent premium to the market price substantially undervalue a company?

That is what Direct Line Group’s board maintains. The UK insurer rejected a £3.3bn offer from Aviva which values its shares at 250p, or at a 57.5 per cent premium to Wednesday’s closing price. Its position nods to the perceived disconnect between share prices on the beleaguered UK stock market and underlying value. But more than anything, it looks like a punchy negotiating tactic.

Direct Line does have a valid conceptual point. It is true that, in the UK, the extra value that a buyer needs to offer to win backing for a takeover has been rising. In local parlance, 40 is the new 30 — indicating that the benchmark premium required to even merit attention has moved up by some 10 percentage points simply to reflect the FTSE’s perceived undervaluation.

On top of this, companies attempting a turnaround can be particularly hard to value. Direct Line was blindsided by a post-Covid surge in the cost of car repairs. Its new-ish chief executive Adam Winslow, hired from Aviva in 2023, has a plan to rebuild margins. But so far, the market has not given him much credit.

Whether one buys into Winslow’s turnaround or not makes a difference. Before Aviva’s offer, Direct Line was trading at a meagre 6.2 times two-year forward earnings, on S&P Capital IQ estimates. Putting it on Aviva’s own multiple would imply a value of more than 220p per share — on which basis the latest bid premium would look much less compelling. It is worth noting that Direct Line successfully defended itself from a 239p-a-share bid from Belgian insurer Ageas earlier this year.

Such considerations may, in part, explain Direct Line’s strongly-worded rebuttal. But clever tactics play just as big a role.

Aviva can clearly extract a lot of value from merging with Direct Line. Strategically it is a good fit, turning Aviva into a top player in personal and motor insurance in the UK. The larger insurer might be able to lop off 20 per cent of Direct Line’s administration costs, think Berenberg analysts, which — taxed and capitalised — would yield an extra £1.1bn of value. On top of that, a tie-in with a larger and more diversified insurer would allow Direct Line to release some regulatory capital.

Direct Line is probably betting that, given the juicy savings on offer, it can squeeze Aviva for a little more before it lets it into the tent. Its shareholders, who bid up the stock by more than 40 per cent on Thursday, will be hoping the insurer has not overplayed its hand.

#Direct #Line #playing #hardball #Aviva #bid