The simple secret behind the UK’s best performing council pension fund

Quentin Marshall, chair of Kensington and Chelsea’s £1.9bn pension scheme, has delivered the best performance of any UK local authority fund over the past decade by parking half of its assets in a global equity index tracker.

Marshall, who has chaired the fund since 2014, said individual stock or fund selection hinders rather than helps drive returns and he avoids tactical decision making when his team meets to review its investments.

“All three of those things, post risks and post costs, definitely do not add value,” he told the Financial Times in an interview at his office in Mayfair.

“The whole asset management industry is built on the premise that they have value,” Marshall said. He is withering in particular about consultants who advise pension funds on investment decisions and “rely on backward looking data which is definitely shown to be completely and utterly useless as a source of prediction”.

Over the past decade, the 51-year-old Conservative party councillor and banker has delivered average annual returns of 10.8 per cent for the pensions of workers at Kensington and Chelsea’s council, which provides services to both the wealthiest parts of the UK and neighbourhoods with significant deprivation.

The performance, driven by a heavy equity exposure, outstrips other local authorities, according to shareholder advisory group PIRC. Marshall’s fund was the only local authority to achieve double digit annual returns over the past decade. The second best was Bromley council, which trailed him with 9.3 per cent.

But Marshall is unlike many of the people who run the patchwork of pension funds for government workers across the country. The councillor for the ward of Brompton is also chief executive at Weatherbys private bank in Mayfair and previously held senior investment roles at Coutts and UBS Wealth Management.

Marshall attributes his performance in part to making few decisions. His team meets formally to review its strategic asset allocation once a year but it has been “broadly unchanged for many years”.

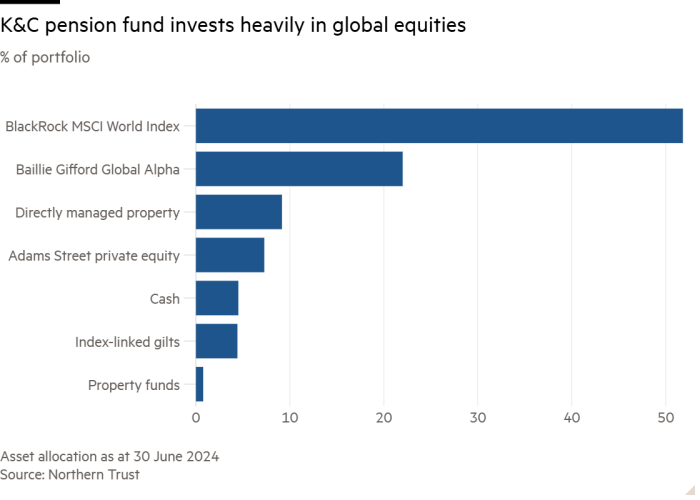

Half of the fund follows the BlackRock MSCI world index tracker, albeit he has made a carve out in his global equity index exposure to exclude three companies linked to the 2017 devastating Grenfell fire in Kensington and Chelsea.

His rejection of fund and stock selection makes him sceptical that the UK government’s decision to pool all of the assets of England and Wales’s £391bn local government pension scheme will help boost pension returns, although he supports the government’s attempts to professionalise the investment process.

Last month Labour chancellor Rachel Reeves set out plans for a series of “megafunds” to run local council pension assets, a move the government hopes will drive billions of pounds of investment into British infrastructure and fast growing companies. The reform programme was supported by her Tory predecessor Jeremy Hunt.

But Marshall does not buy their argument that the reforms will lead to better pension returns for cash strapped councils.

“This has nasty overtones of PPP to me,” said Marshall, referring to public-private partnerships that boomed in the late 1990s and early 2000s and were widely considered to deliver poor value to the public purse.

“All governments of all stripes have a massive temptation to move overt spending from the public eye . . . but if it truly were an investment you wouldn’t need to tell us to do it,” he said.

“Is this money for discharging pension liability or is it a fund for government to spend . . . I think they are sorely tempted to change it from the former to the latter,” Marshall added.

The Kensington and Chelsea pension fund does not have any allocation to infrastructure. Marshall said he had looked at infrastructure “closely” but had chosen not to invest owing to “very high manager fees, very little diversification in comparison to liquid securities markets and limited upside versus existing asset classes in terms of return”.

As the government pushes consolidation of local authority pension assets, Marshall said it was “absolutely fundamental” that strategic asset allocation decisions remain with the local authorities, because they remain responsible for ensuring that pensions are paid. Different councils have different risk tolerances depending on the level of funding of their pension scheme, contribution rates and the demography of scheme members.

The government has signalled that it will allow decisions for “a high-level strategic asset allocation” to remain with local councils, but said in a consultation it believes that expertise in the pools make them best placed to take on the task.

“If you were to divorce strategic asset allocation from the underlying liability structure you would have a real problem — the chain of accountability is really important,” Marshall said.

Kensington and Chelsea is in the process of building up its property portfolio, with a target asset allocation of 75 per cent in equities, 20 per cent in property and 5 per cent in index-linked bonds.

The council’s scheme has a funding level of over 200 per cent, meaning it estimates it can pay twice as much as the pensions owed.

As a consequence, contribution rates into the pension have been reduced, freeing up more money for the council to spend on local services.

While Marshall has some sympathy for the government’s move to take investment decisions out of the hands of councillors, who rely on advice from pension consultants, he hopes that the government will leave enough flexibility in the system so “sensible people” can disagree.

“Anything that is too rigid and too doctrinaire is I think likely to lead to poor outcomes and citizens should care about this because it’s £400bn of assets . . . this is real money that will have a real impact on whether your local library will stay open and grandmother gets good care,” he said.

#simple #secret #UKs #performing #council #pension #fund