FedEx looks to deliver value by uncoupling freight trucking division

Unlock the Editor’s Digest for free

Roula Khalaf, Editor of the FT, selects her favourite stories in this weekly newsletter.

Corporate spin-offs are all the rage.

FedEx is the latest to jump on the bandwagon. The US logistics group plans to split out its higher margin freight trucking division into a separate publicly listed company. While the move should unlock immediate gains for shareholders, it won’t tackle FedEx’s bigger problem: falling volumes at its core parcel delivery business as it battles intense competition from UPS, Amazon, Uber and others.

More big companies are exploring break-ups as investors (again) sour on sprawling conglomerates — Honeywell is another recent example. There are good reasons driving the trend. Spin-offs allow the parent company to run leaner and more focused operations while the newly established group can pursue its own growth strategies. They also have the added benefit of being more tax efficient. Unlike a direct sale, they are usually tax-free.

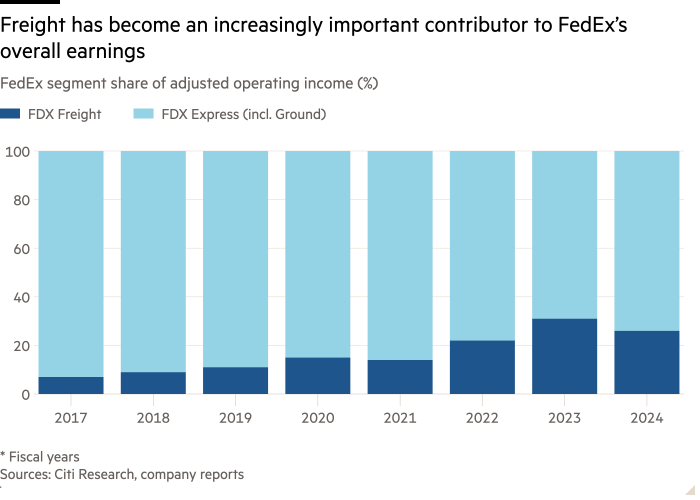

In FedEx’s case, back-of-the-envelope arithmetic shows why making freight an independent company stacks up. The unit is a “less-than-truckload” business, meaning it picks up small loads from customers and combines them to fill a truck. It is FedEx’s most profitable business. The $9.4bn in revenue the unit pulled in last year accounted for just 10 per cent of group sales but generated a third of group operating income. Yet this is not fully reflected in FedEx’s valuation of just 13 times forward earnings. Pure-play freight companies such as XPO and Old Dominion Freight Line trade on a multiple of about 33 times.

Apply that same multiple to FedEx Freight and the business could be worth as much as $43bn as a standalone company. However, Freight is unlikely to fetch that premium valuation, given that its topline growth is slower than that of its competitors. In fact both revenue for the division fell 7 per cent and margins shrank in the six months to the end of November. Analysts at Citi reckon a more reasonable equity value for the unit would be between $30bn to $35bn. FedEx, whose shares are up 9 per cent this year, has a market value of $66bn.

The devil will also be in the detail. FedEx aims to complete the spin-off in 18 months. What is unclear is how much debt the new company will be saddled with and whether current Freight customers will defect to rivals. Also, unclear is how FedEx will turn around its remaining Ground and Express delivery businesses without revenue from Freight to subsidise its efforts. These two are low margin businesses, which will require plenty of capital investment. A spin-off is no guarantee to deliver results over the long term.

#FedEx #deliver #uncoupling #freight #trucking #division