BHP did Anglo American a favour

Unlock the Editor’s Digest for free

Roula Khalaf, Editor of the FT, selects her favourite stories in this weekly newsletter.

Happy BHP day! From midnight tonight, the Australian miner is free under UK market rules to make another bid for Anglo American, after the latter spurned a complex £39bn all-share offer in May.

But whether BHP returns — or another suitor appears — one thing is clear: the frenetic six-week pursuit earlier this year has already given Anglo a leg-up.

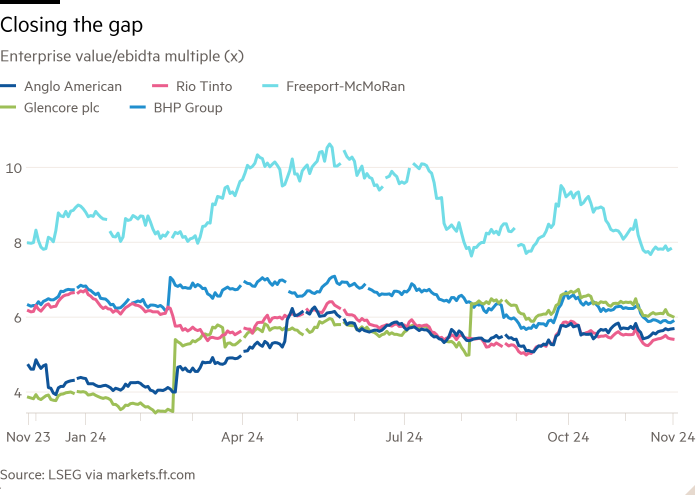

Shares in the London-listed group have outperformed since April (BHP made its opening offer on the 25th of that month). Its shares are up 16 per cent compared with falls at peers including BHP, Rio Tinto and Glencore. More impressive, that has come against weakness in the prices of key commodities such as iron ore.

There is still a yawning valuation gap with copper specialists such as Freeport-McMoRan and Antofagasta, on an average 8 times EV/ebitda multiple. But Anglo — whose discount to peers over the past decade has been close to 15 per cent — is gaining ground. It trades on a multiple of around 5.7 times on S&P Capital IQ data; a year ago this was 4.6.

Partly, Anglo has been lifted by speculation of another bid. But Anglo’s chief executive Duncan Wanblad can take some credit here. After unveiling a radical break-up as part of his BHP defence in May, Wanblad has shown he can execute. Anglo’s reputation had been the opposite: the miner has repeatedly disappointed on promises to hack back its portfolio.

Wanblad has announced two deals through which the entirety of Anglo’s steelmaking coal business will be sold for a total of up to $4.9bn (which includes payments contingent on certain milestones). But even the minimum of $3.6bn Anglo will get is good, suggests UBS’s Myles Allsop. A UBS investor survey earlier this month had indicated they were looking for $3bn-$4bn.

True, the trickier parts of Wanblad’s restructuring are still to come as he tries to refocus the group on copper, iron ore and fertilisers. Not least, a trade sale or IPO of De Beers will be tough in a diamond market that is under severe pressure from lab-grown stones and the luxury slowdown in China.

But again, the BHP approach has helped with another of Anglo’s trickier carve-outs. Anglo has twice sold down shares in Johannesburg-listed Anglo American Platinum, leaving a spinout on track by the middle of next year. Concern in South Africa about BHP’s interest has probably helped Anglo move quickly on its own restructuring plans.

Wanblad’s work may simply make Anglo more attractive to a potential suitor. Investors are better off, regardless. And he may even do enough for Anglo to think about some hunting of its own.

#BHP #Anglo #American #favour